When he was selected to pursue a Bachelor of Arts, Industrial, and Organisational Psychology degree at �the university God loved the most� in 1999, Noel Chowawa had a glimmer of hope.

His parents could not afford the tuition fees at the time, especially since two of his siblings were already in university.

The need was enormous, he says, and for him, going to school meant constraining the family�s already meagre financial base further�especially since it had a single revenue stream; his father�s salary.

�Having three university students besides supporting my other siblings in Secondary School took a huge toll on my family. And, in my family, only my father had a source of income,� Chowawa recalls.

Chowawa was, at the time, seeing his dream of graduating from Chanco, as the University of Malawi (then Chancellor College) was fondly called, narrowly escaping off his hand.

But not until Noel�s name and that of his sister were on the list of university loan beneficiaries�a government loan facility aimed at aiding deserving public and private university students to access higher education despite their financial limits.

�We were also given book and stationary allowances through the same facility which made life easy for us,� he says.

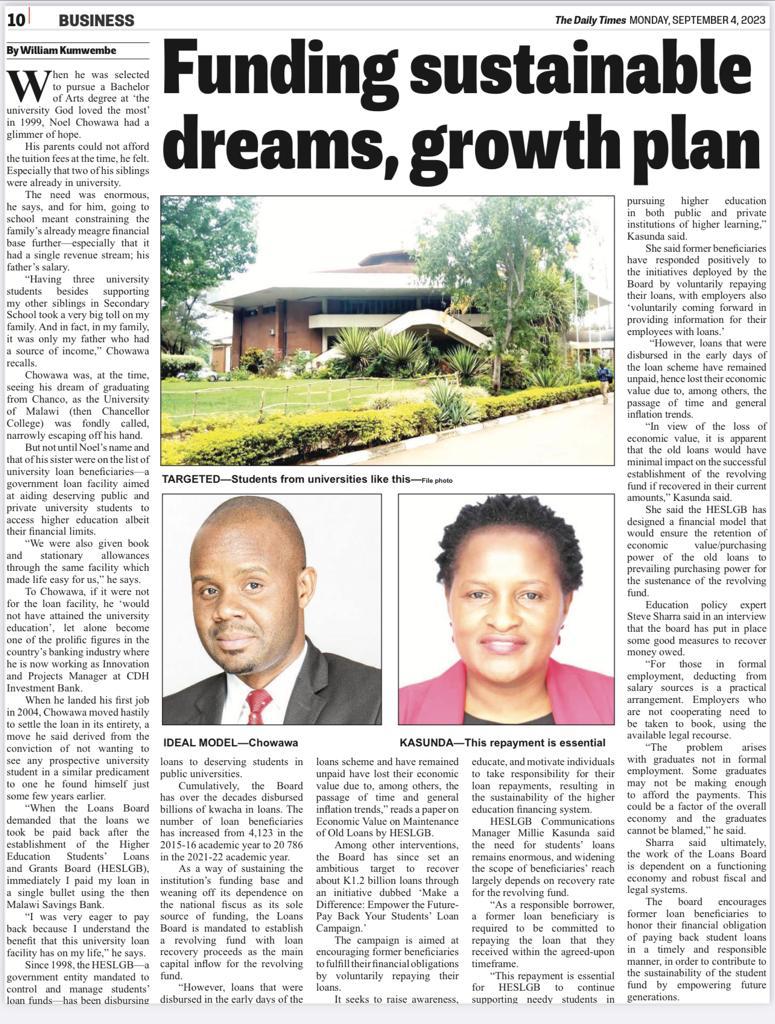

To Chowawa, if it were not for the loan facility, he �would not have attained the university education�, let alone become one of the prolific figures in the country�s banking industry where he is now working as Innovation and Projects Manager at CDH Investment Bank.

When he landed his first job in 2004, Chowawa moved hastily to settle the loan in its entirety, which he said derived from the conviction of not wanting to see any prospective university student in a similar predicament to one he found himself just some few years earlier.

�When the Loans Board demanded that the loans we took, be paid back after the establishment of the Higher Education Students� Loans and Grants Board (HESLGB), immediately I paid my loan in a single bullet using the then Malawi Savings Bank.

�I was very eager to pay back because I understand the benefit that this university loan facility has on my life,� he says.

Since 1998, the HESLGB�a government entity mandated to control and manage students� loan funds�has been disbursing loans to deserving students in public universities.

Cumulatively, the Board has over the decades disbursed billions of kwacha in loans. The number of loan beneficiaries has increased from 4,123 in the 2015-16 academic year to 20,786 in the 2021-22 academic year.

As a way of sustaining the institution�s funding base and weaning off its dependence on the national fiscus as its sole source of funding, the Loans Board is mandated to establish a revolving fund with loan recovery proceeds as the main capital inflow for the revolving fund.

�However, loans that were disbursed in the early days of the loans scheme and have remained unpaid have lost their economic value due to, among others, the passage of time and general inflation trends,� reads a paper on Economic Value on Maintenance of Old Loans by HESLGB.

Among other interventions, the Board has since set an ambitious target to recover about K1.2 billion loans through an initiative dubbed �Make a Difference: Empower the Future-Pay Back Your Students� Loan Campaign.�

The campaign is aimed at encouraging former beneficiaries to fulfil their financial obligations by voluntarily repaying their loans.

It seeks to raise awareness, educate, and motivate individuals to take responsibility for their loan repayments, resulting in the sustainability of the higher education financing system.

HESLGB Communications Manager Millie Kasunda said the need for student loans remains enormous, and widening the scope of beneficiaries� reach largely depends on the recovery rate for the revolving fund.

�As a responsible borrower, a former loan beneficiary is required to be committed to repaying the loan that they received within the agreed-upon timeframe.

�This repayment is essential for HESLGB to continue supporting needy students in pursuing higher education in both public and private institutions of higher learning,� Kasunda said.

She said former beneficiaries have responded positively to the initiatives deployed by the Board by voluntarily repaying their loans, with employers also �voluntarily coming forward in providing information for their employees with loans.�

�However, loans that were disbursed in the early days of the loan scheme have remained unpaid, hence lost their economic value due to, among others, the passage of time and general inflation trends.

�Because of the loss of economic value, it is apparent that the old loans would have minimal impact on the successful establishment of the revolving fund if recovered in their current amounts,� Kasunda said.

She said the HESLGB has designed a financial model that would ensure the retention of economic value/purchasing power of the old loans to prevailing purchasing power for the sustenance of the revolving fund.

Education policy expert Steve Sharra said in an interview that the board has put in place some good measures to recover money owed.

�For those in formal employment, deducting from salary sources is a practical arrangement. Employers who are not cooperating need to be taken to book, using the available legal recourse.

�The problem arises with graduates who are not in formal employment. Some graduates may not be making enough to afford the payments. This could be a factor in the overall economy and the graduates cannot be blamed,� he said.

Sharra said ultimately, the work of the Loans Board is dependent on a functioning economy and robust fiscal and legal systems.

The Board encourages former loan beneficiaries to honour their financial obligation of paying back student loans in a timely and responsible manner and to contribute to the sustainability of the student fund by empowering future generations.

Post a comment